Over 1,000 Furniture Stores Are Closing -- Who Will Be the Real Estate and Market Share Winners?

3 MM+ Square Feet and $2 BB in Annual Furniture Sales Will Be Up For Grabs As A Result Of Store Closures By Conn's and Big Lots

In 2001 Sears HomeLife Furniture — which had 128 stores and annual sales of ~$700 MM — filed for bankruptcy and closed all of its stores.

But most of the HomeLife Furniture stores did not remain vacant for long — and many continued to operate as furniture stores for years.

Havertys Furniture paid $11 million to acquire four of HomeLife Furniture’s Central Florida stores and three other leased locations.

The HomeLife store additions increased the number of Havertys showrooms by 10%.

Bob’s Discount Furniture — which had operated only 15 stores at the time — acquired three of the HomeLife sites in Massachusetts and New Hampshire

The real estate and leases for over two dozen other HomeLife stores in multiple states were also acquired by regional furniture chains and reopened as furniture stores.

So not only was much of the HomeLife real estate quickly re-tenanted, but most of the new tenants were also other furniture stores.

A similar situation happened ~20 years later in Michigan.

In March 2020 Art Van Furniture — the largest privately held furniture company in Michigan with ~$700 MM in annual sales — filed for bankruptcy.

All 85 of its corporate-owned Michigan stores ultimately closed for good.

But ~90% of the former Art Van stores in Michigan were re-occupied within three years — and 70% of the new tenants were furniture and mattress stores.

Like with HomeLife, the Art Van bankruptcy and liquidation resulted in a unique real estate and market share opportunity for its competitors.

And regional operators such as Gardner White Furniture and ABC Warehouse — as well as national chains like Value City Furniture, Ashley HomeStore, Sleep Number and Mattress Firm — stepped into much of the Art Van real estate in an attempt to capture its $700 MM in annual furniture sales.

Now a similar real estate and market share opportunity is again presenting for furniture retailers.

Conn's, a Houston-based furniture and appliance retailer with ~$1.2 BB in annual revenue, filed for Chapter 11 bankruptcy last month with plans to close its 170 Big Box stores and the 380 stores operated by its Badcock Furniture subsidiary.

And Big Lots — where furniture and mattress sales account for 1/4 of sales and $1 BB in annual revenue — is closing up to 315 of its stores and is reportedly considering a bankruptcy filing that could result in more than 1,000 additional store closures.

As the HomeLife and Art Van Furniture cases demonstrated, furniture store bankruptcies have been a strategic real estate, market share and growth opportunity for surviving furniture chains.

But furniture retailers have also benefited from other Big Box retail bankruptcies.

For instance, Havertys Furniture is opening five new stores in 2024 — all of which were former Bed Bath & Beyond sites vacated after its 2023 bankruptcy.

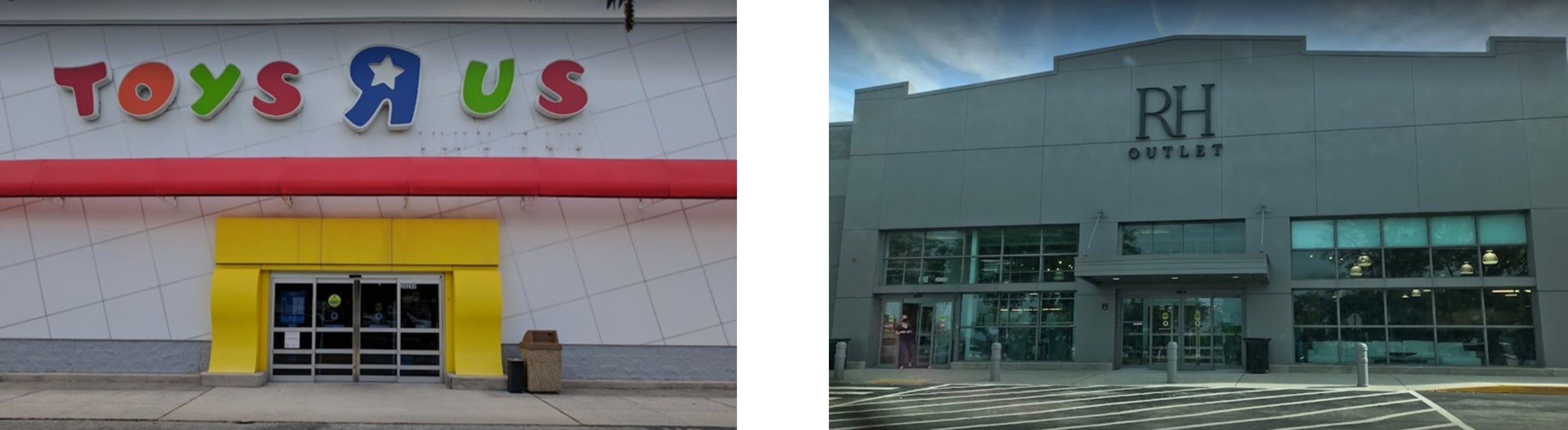

Several furniture retail chains backfilled the ~730 Big Box store closures following the 2017 bankruptcy of Toys R Us.

Approximately 20% of Toys R Us stores — over 130 in total — were re-tenanted by furniture retailers such as Ashley HomeStore, Raymour & Flanigan, Scandanavian Designs and even RH which opened outlet stores at multiple Toys R Us sites.

Bob’s Discount Furniture — which had just 15 stores when it acquired former HomeLife sites two decades ago — moved into at least 20 former Toys R Us stores.

Former Toys R Us sites account for more than 10% of the Company’s 177 furniture stores in 24 states — and roughly 1 out of every 3 of the growing chain’s 60+ new store openings over the past five years has been in a former Toys R Us store.

Now the impending store closures by Conn’s and Big Lots will likely result in a similar real estate and market share opportunity for furniture store chains.

The 170 stores operated by the Conn's brand are between 25,000 and 35,000 square feet on average and are located in 15 states — mostly the Southern and Western U.S. — where there is limited Big Box vacancy.

The Conn’s stores are generally in good condition, adjacent to other retailers, and suitable for many uses.

But they have been "known" furniture destinations for years.

Plus the stores are already built out for a furniture sales, so few improvements would be necessary for other furniture retailers to be up and running at the sites.

So — as with the previous HomeLife and Art Van Furniture cases — the Conn's real estate could provide its former competitors with a unique opportunity to quickly and profitably grow their business and absorb the lost furniture sales at its stores.

The Big Lots real estate may also provide a similar opportunity — though there are some key differences from the Conn’s stores.

Unlike the more regionalized Conn’s, Big Lots stores are located across the country — in every state except Alaska and Hawaii — and in both suburban and rural areas.

Additionally, furniture accounts for only ~1/4 of sales at Big Lots — and its lower volume stores may not offer significant market share capture for furniture retailers.

But the size of the Big Lots stores — between 30,000 and 40,000 square feet — may still be attractive to furniture chains, particularly in high barrier-to-entry markets.

Ultimately if the 1,000 (or more) former Conn’s and Big Lots stores are quickly re-tenanted, furniture retailers are likely to be among the most likely takers of the space.

And even as the Conn’s and Big Lots brands fade away like HomeLife and Art Van before them, their real estate may still be used for furniture sales for years to come!