Over 1,500 Furniture Stores And 35 MM Square Feet Is Being Vacated By Bankrupt Furniture Retailers -- What Are The Best Tenant Fits For The Real Estate?

35 MM+ Square Feet Is Up For Grabs Following Store Closures By Conn's, Big Lots and American Freight

The Big Box retailer category with the most 2024 bankruptcies and store closures?

Furniture stores.

In just the last three months three major furniture retailers — Conn’s, Big Lots and American Freight — have filed for bankruptcy.

These bankruptcies are expected to result in at least 1,500 store closures and over 35 MM square feet of vacancy.

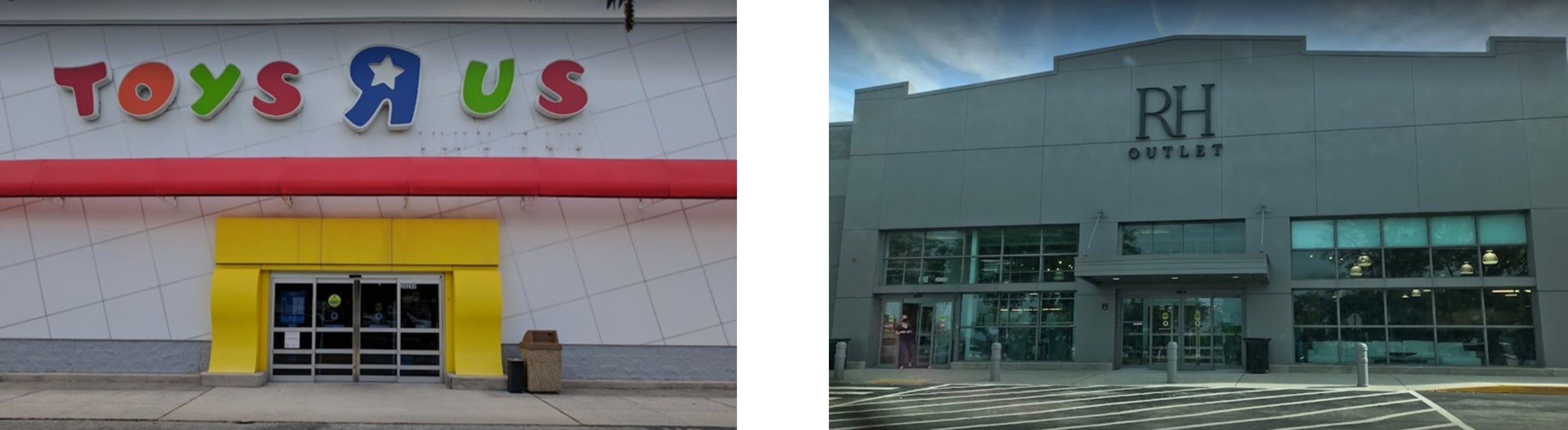

To put that in perspective, these furniture store closures are more than twice the ~725 Toys R Us sites and over three times the ~480 Bed Bath & Beyond stores that closed during the bankruptcies of those two retailers.

The Toys R Us and Bed Bath & Beyond real estate, however, happened to be very much in demand by other users.

In fact ~90% of the Toys R Us sites had new tenants in just three years — and over 1/2 of the 480+ Bed Bath stores have already been backfilled in the 18 months after its April 2023 bankruptcy.

Now the recent furniture retailer bankruptcies have resulted in a similar real estate opportunity:

Conn's, a Houston-based furniture and appliance retailer with ~$1.2 BB in annual revenue is closing its 170 Big Box stores and the 380 stores operated by its Badcock Furniture subsidiary which collectively total over 12 MM square feet.

Big Lots — where furniture and mattress sales account for 1/4 of sales and $1 BB in annual revenue — filed for bankruptcy in September is closing at least 500 stores and vacating over 14 MM square feet.

American Freight, a subsidiary of the Franchise Group which went bankrupt in early November, is closing 329 stores that total over 9 MM square feet and generate ~$900 MM in annual revenue.

So how much of this space will be absorbed and who are the likely takers of the space?

Several growing retailers have already acquired some of this vacated real estate.

Burlington Stores has successfully bid to purchase 15 Conn’s leases and 13 Big Lots leases.

But this is nothing new for Burlington as it had previously re-tenanted over 55 former Toys R Us stores and more than 60 former Bed Bath & Beyond suites.

Similarly, Ollie’s Bargain Outlet acquired 15 Big Lots leases.

Like Burlington, Ollie’s has backfilled a number of stores vacated by bankrupt retailers. In fact, former Toys R Us and Kmart buildings account for roughly 20% of its current store base.

Regional and national furniture chains are also likely to take full advantage of this available real estate and market share.

Furniture retailers backfilled a significant amount of the real estate vacated by Toys R Us and Bed Bath & Beyond.

Roughly 20% of Toys R Us stores — over 130 in total — were re-tenanted by furniture retailers such as Ashley HomeStore, Raymour & Flanigan and Scandinavian Designs.

Even luxury home furnishings company RH opened outlet stores at multiple former Toys R Us sites.

Bob’s Discount Furniture moved into at least 20 former Toys R Us stores and nearly 1 out of every 3 of the growing chain’s 60+ new store openings over the past five years was in a former Toys R Us.

Toys R Us sites now account for more than 10% of the 177 Bob’s Discount Furniture stores in 24 states.

The Bed Bath & Beyond real estate has also been a source of opportunity for expanding furniture retailers.

Havertys Furniture opened five new stores in 2024 — all of which were former Bed Bath & Beyond sites vacated after its 2023 bankruptcy.

But the impending store closures by Conn’s, Big Lots and American Freight represent not only additional real estate options for furniture store chains — but also an “instant” expansion and market share capture opportunity for furniture store chains.

Like for Royal Furniture, a Memphis-based furniture retailer that was founded in 1946 and operates 12 furniture stores in Tennessee, Mississippi and Alabama.

Last month Royal acquired the leases to 14 Badcock Furniture stores in Tennessee and Alabama. These new Royal Furniture “dealership” stores will more than double its store base overnight.

The 170 stores operated by the Conn's brand are between 25,000 and 35,000 square feet on average and are located in 15 states — mostly the Southern and Western U.S. — where there is limited Big Box vacancy.

The Conn’s stores are generally in good condition, adjacent to other retailers, and suitable for many uses.

But they have been "known" furniture destinations for years and have generated over $7 MM in revenue per store.

Plus the stores are already built out for a furniture sales, so few improvements would be necessary for other furniture retailers to be up and running at the sites — and attempt to capture the lost Conn’s sales.

The Big Lots real estate may also provide a similar opportunity — though there are some key differences from the Conn’s stores.

Unlike the more regionalized Conn’s, Big Lots stores are located across the country — in every state except Alaska and Hawaii — and in both suburban and rural areas.

Additionally, furniture accounts for only ~1/4 of sales at Big Lots — and its lower volume stores may not offer significant market share capture for furniture retailers.

But the size of the Big Lots stores — between 30,000 and 40,000 square feet — may still be attractive to furniture chains, particularly in high barrier-to-entry markets.

The latest furniture retail closures will come courtesy of the 329 American Freight stores that are now also being liquidated.

American Freight’s parent company, the Franchise Group, filed for bankruptcy protection on November 3rd and immediately moved to wind down the American Freight chain citing sustained inflation and macroeconomic challenges.

The American Freight stores are 28,000 square feet on average and generated approximately $4 MM in annual sales on average.

The stores are located urban, suburban and rural areas across 40 states — and might also be a good opportunity for regional and independent furniture stores and chains to relocate or expand.